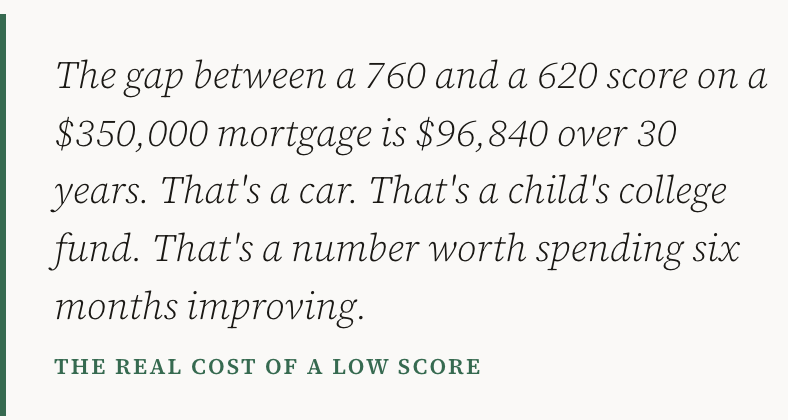

Picture two buyers. Same city, same home, same $350,000 loan. They apply for mortgages on the same day from the same lender. Buyer A has a credit score of 760. Buyer B has a score of 660. Buyer A gets a rate of 6.50%. Buyer B gets 7.65%. That 1.15-point difference produces a monthly payment gap of $249. Over 30 years, Buyer B pays $89,640 more for the exact same house.

Not because they bought a worse home. Not because they found a worse lender. Simply because of a three-digit number they may have never looked at carefully.

Your credit score is the single most controllable variable in what your mortgage actually costs you. And most buyers don't know the exact numbers — what each tier costs, how to move between them, and how much time a meaningful improvement actually takes.

This post fixes that. By the end, you'll know exactly where you stand, what it costs, and what to do about it before you ever talk to a lender.

Published June 1, 2026

How Your Credit Score Affects Your Mortgage — By the Exact Numbers

The five tiers lenders actually use

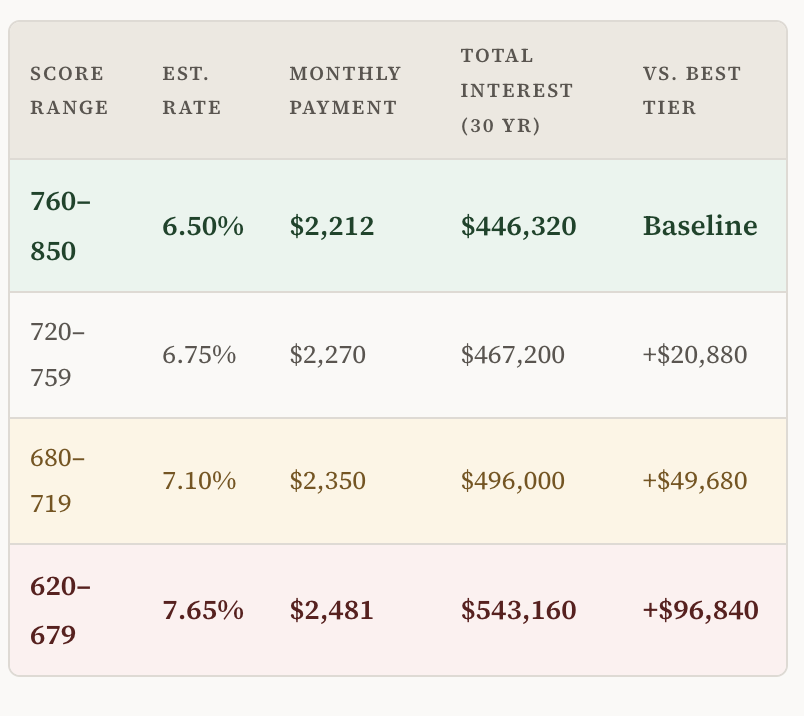

When you apply for a mortgage, lenders don't see a single credit score. They pull reports from all three bureaus — Equifax, Experian, and TransUnion — and typically use the middle score of the three for underwriting. It's also worth knowing that mortgage lenders use older FICO scoring models (FICO 2, 4, and 5) rather than the FICO 8 you'd see on Credit Karma. The two numbers can differ by 20–40 points.Internally, most lenders sort borrowers into pricing tiers that look roughly like this:

Crossing from one tier into the next is what generates meaningful rate changes. Moving from 718 to 722 doesn't just add 4 points — it puts you in a different pricing bucket entirely. That's why knowing your exact number, and knowing exactly what score you're targeting, matters so much.

The exact numbers: rate, payment, and lifetime cost by tier

The table below uses a $350,000 loan, 30-year fixed rate, with estimated rates that reflect 2026 market conditions. These are illustrative — your actual rate will depend on your lender, loan type, and down payment — but the relationships between tiers are consistent across the market.

Illustrative figures based on 2026 market conditions. Actual rates vary by lender, loan type, and down payment.

What actually makes up your score

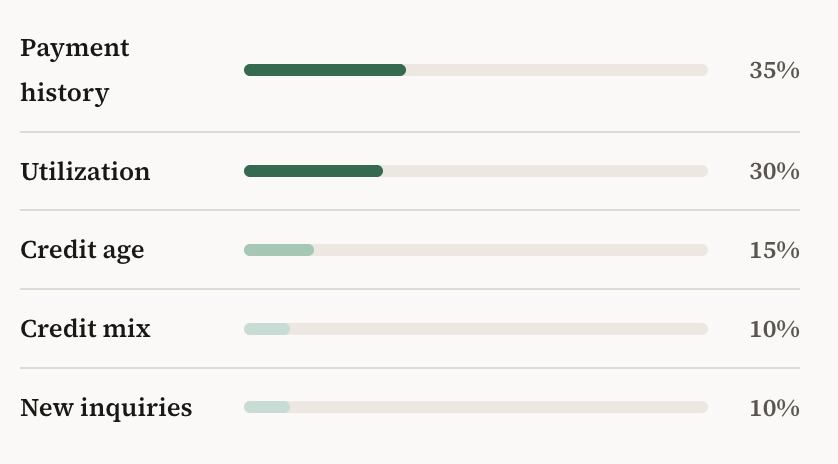

Understanding the five factors that build your FICO score — and how heavily each one is weighted — tells you exactly where to focus your effort.

Payment history (35%): This is the most important factor and the one you have the least ability to fix quickly. A single 30-day late payment can drop a score by 60–110 points and stays on your report for seven years. If you have late payments, you can't erase them — but you can bury them under a consistent streak of on-time payments going forward.

Credit utilization (30%): This is the fastest factor to move. Utilization is how much of your available revolving credit you're using at any given time. The common advice is to stay under 30%, but that's not good enough for top-tier scores. Borrowers in the 760+ range typically carry under 10% utilization. If you have a $10,000 credit limit across all cards, that means carrying no more than $1,000 in balances when your statements close.

Credit age (15%): The longer your accounts have been open, the better. This is why closing old credit cards — even ones you don't use — is almost always a mistake. That rarely-used card from 2015 is doing silent, invisible work for your score every month. Leave it open.

Credit utilization (30%): This is the fastest factor to move. Utilization is how much of your available revolving credit you're using at any given time. The common advice is to stay under 30%, but that's not good enough for top-tier scores. Borrowers in the 760+ range typically carry under 10% utilization. If you have a $10,000 credit limit across all cards, that means carrying no more than $1,000 in balances when your statements close.

Credit age (15%): The longer your accounts have been open, the better. This is why closing old credit cards — even ones you don't use — is almost always a mistake. That rarely-used card from 2015 is doing silent, invisible work for your score every month. Leave it open.

Common mistakeClosing a credit card before applying for a mortgage feels responsible. It's actually one of the fastest ways to drop your score. It reduces your available credit (raising utilization) and can lower your average account age. Leave old accounts open unless there's a compelling fee reason not to.

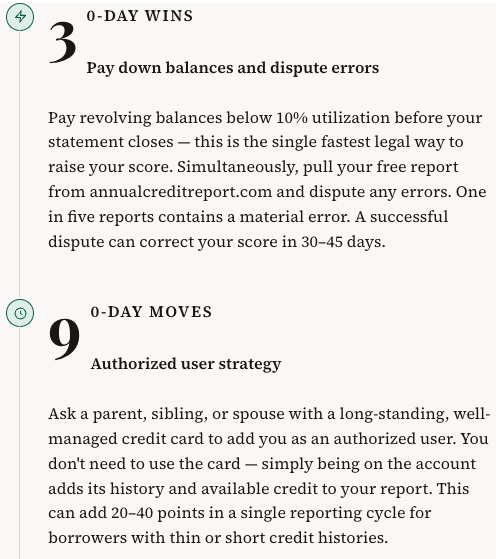

New inquiries (10%): When a lender pulls your credit, it creates a "hard inquiry" that slightly dings your score. But here's the important exception: FICO treats all mortgage-related hard inquiries that occur within a 45-day window as a single inquiry. This means you can and should apply to multiple mortgage lenders to compare rates without worrying about damaging your score each time.The fastest ways to move your score before you apply

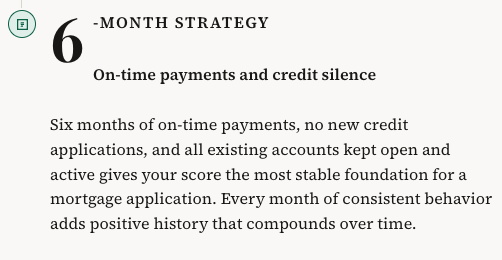

Credit improvement isn't mysterious — but it does take time, and different actions work on different timelines. Here's what to do based on how far out you are from applying.

One tool most buyers don't know about: free score simulators available through your bank or through services like Credit Karma. These let you model the impact of specific actions — paying off a specific card, disputing an error, adding an account — before you take them. Use them.

The tradeoff is mortgage insurance premiums (MIP): an upfront fee of 1.75% of the loan amount, plus an ongoing annual premium that typically runs 0.55–1.05% of the loan balance. On a $350,000 loan, that's roughly $160–$300 added to your monthly payment — and unlike private mortgage insurance on conventional loans, FHA MIP doesn't automatically cancel when you reach 20% equity if your down payment was below 10%.

When does FHA make sense? When the alternative is waiting 12–18 months while paying rent that's rising every year. The math won't always favor waiting, even if the FHA rate and insurance cost slightly more. Run both scenarios with real numbers before deciding.

How to protect your score during the mortgage process

Once you've built your score up, the application process itself carries its own risks. Here's what to avoid in the 60–90 days before closing.Protect your scoreDo not open any new credit accounts, make large purchases on existing cards, co-sign for anyone else's loan, or allow any unnecessary hard inquiries during the mortgage process. Lenders typically pull your credit a second time right before closing. Any significant change discovered between application and closing can delay or derail your loan.

Apply to multiple lenders within a 45-day window to rate shop safely. Before any lender pulls your report, pull your own first — it's a soft inquiry that has zero impact on your score. Knowing your number before they do means no surprises.When a lower score still gets you a home: the FHA option

For buyers with scores below 640, conventional loans become expensive or unavailable. FHA loans — insured by the Federal Housing Administration — allow scores as low as 580 with a 3.5% down payment, or 500 with 10% down.The tradeoff is mortgage insurance premiums (MIP): an upfront fee of 1.75% of the loan amount, plus an ongoing annual premium that typically runs 0.55–1.05% of the loan balance. On a $350,000 loan, that's roughly $160–$300 added to your monthly payment — and unlike private mortgage insurance on conventional loans, FHA MIP doesn't automatically cancel when you reach 20% equity if your down payment was below 10%.

When does FHA make sense? When the alternative is waiting 12–18 months while paying rent that's rising every year. The math won't always favor waiting, even if the FHA rate and insurance cost slightly more. Run both scenarios with real numbers before deciding.

Most people treat their credit score the way they treat the weather — something that happens to them, not something they control. But unlike the weather, a credit score responds predictably to specific actions taken over specific periods of time.

Every point you move your score is money you keep. And the math, as you've now seen, makes the effort very much worth it.

Every point you move your score is money you keep. And the math, as you've now seen, makes the effort very much worth it.

Ready to take the next step?