Categories

RentersPublished May 31, 2026

Why 2026 Is the Year Renters Finally Buy

Maria has lived in the same two-bedroom apartment for five years. She loves the neighborhood, knows the barista at the corner coffee shop by name, and has painted every room exactly the color she wanted — only to repaint it back to "landlord beige" before each lease renewal. Her rent started at $1,750. This year it hit $2,490.

Last spring, her landlord slid a notice under her door: another $180 increase, effective in 90 days.

That evening, Maria sat down with a mortgage calculator for the first time and did something she hadn't done in years. She ran the numbers. And for the first time, they made sense.

She isn't alone. Across the country, millions of long-term renters are quietly arriving at the same moment — the moment when buying stops feeling impossible and starts feeling urgent. And in 2026, the conditions that create that moment have finally come together all at once.

Mortgage rates came down — but not in the way you think

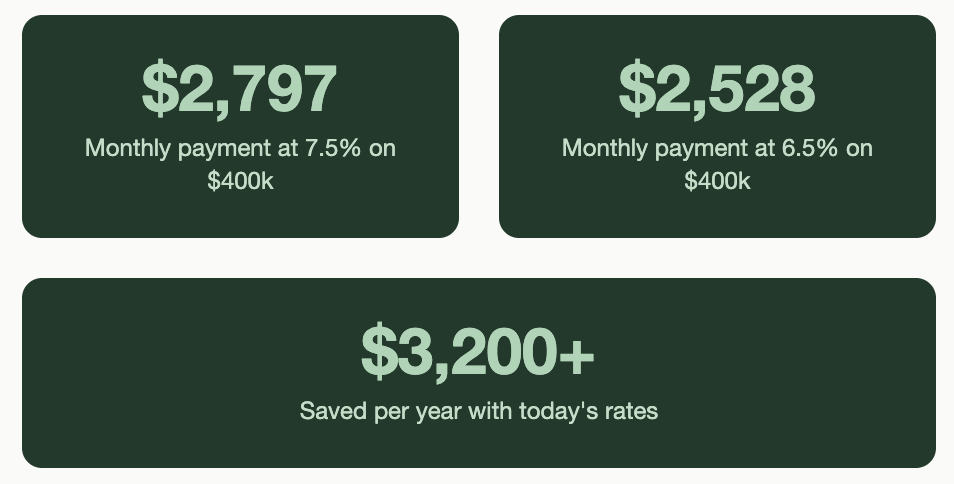

Everyone remembers 2022. Rates that had sat comfortably below 4% for years shot past 7% in a matter of months, then flirted with 8% in 2023. For buyers who'd been saving and planning, it felt like the floor had been ripped out. Monthly payments on a $400,000 home jumped by more than $900. Overnight, millions of people who could afford to buy simply couldn't anymore.

But the rate story in 2026 isn't just about where rates are today — it's about what high rates did to the entire market for three years.

When rates spiked, sellers froze too. Homeowners who'd locked in 3% mortgages in 2020 and 2021 refused to sell and trade up into a 7% loan. This "lock-in effect" strangled inventory. Fewer homes on the market meant the homes that did list sold fast, often over asking, in cash-heavy bidding wars that priced out the very first-time buyers who needed those entry-level homes most.

That cycle is finally breaking. Rates have eased enough — not dramatically, but meaningfully — to cross the psychological threshold that unlocks seller behavior. More sellers are listing. More move-up buyers are moving. The logjam is clearing.

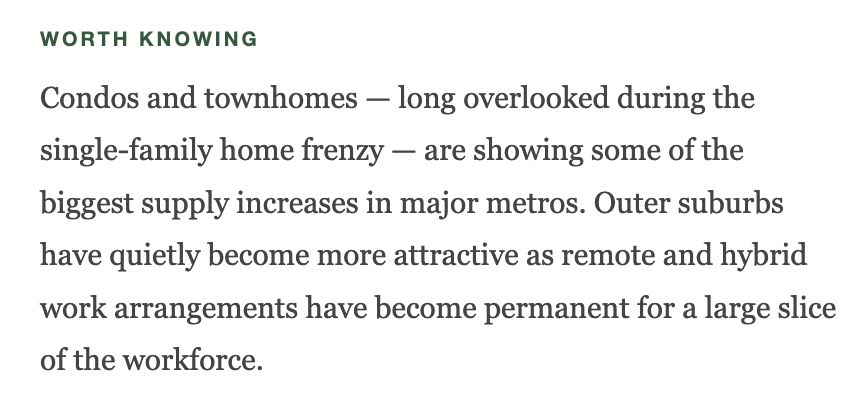

Inventory is finally creeping back — and first-time buyers are first in line

Here's a number worth knowing: builders broke ground on roughly 1.4 million new housing units in 2023 and 2024 combined. Most of those homes are hitting the market right now.

That matters enormously for first-time buyers, because new construction behaves differently from the existing home market. There are no sellers with emotional attachment to a price. There are no bidding wars over memories. Builders want to move inventory, and in 2026, many of them are offering incentives that amount to free money: rate buydowns, closing cost assistance, and upgraded finishes at no charge.

More options means less panic. Less panic means better decisions. That alone changes everything.

Renting got expensive enough to make buying look rational

For years, the standard advice was that renting offered flexibility while buying built wealth. What nobody told renters is that "ready" is a moving target when rents rise 8% a year and buying costs stay relatively fixed.

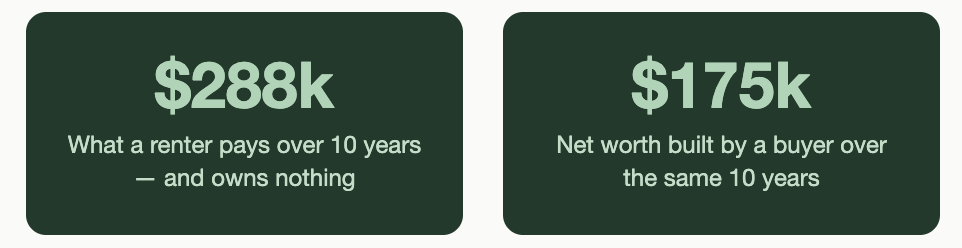

Consider a renter paying $2,400 per month — a reasonable figure in many mid-size cities. That's $28,800 a year in housing costs. Every dollar goes to the landlord. There is no equity. There is no tax deduction.

Now consider a buyer who puts 5% down on a $350,000 home. At today's rates, the all-in payment lands around $2,600 — slightly more than renting. But that extra amount buys roughly $600 a month in equity, mortgage interest deductions, protection from rent increases forever, and an asset that has historically appreciated 3–5% annually.

Down payment programs have never been more generous

The single biggest myth keeping renters from buying is the 20% down payment. It persists in casual conversation, in well-meaning advice from parents who bought in a different era.

In 2026, several state down payment assistance programs have been expanded, funded by federal housing initiatives aimed at closing the homeownership gap. Most first-time buyers have never heard of them.

There's a catch: DPA funds are limited. Programs routinely run out of money partway through the year. The buyers who act early get the grants. The buyers who wait until they feel "completely ready" often find the window has closed.

The honest counterarguments — and why they still don't win

"What if prices drop after I buy?"

They might. Nobody knows. But consider the alternative: waiting for a price drop while paying rent that compounds upward every year. If prices fall 5% and you saved by waiting, but you paid $2,400 a month in rent for 18 months while waiting, you paid $43,200 to save roughly $17,500.

"I might need to move in a few years."

This is the most legitimate concern. Buying works best when you stay for at least three to five years. But if you've been in the same city for years and are using uncertainty as a reason to delay, it's worth examining that honestly.

"My credit isn't ready."

The median credit score for approved mortgages in 2025 was around 720 — but FHA-backed loans have been approved with scores in the 580–620 range. Six to twelve months of on-time payments and reduced utilization can move a score dramatically.

The real cost of waiting is compound. Every year you delay is another year of building someone else's equity, another lease renewal, another rent increase you have no power to refuse.

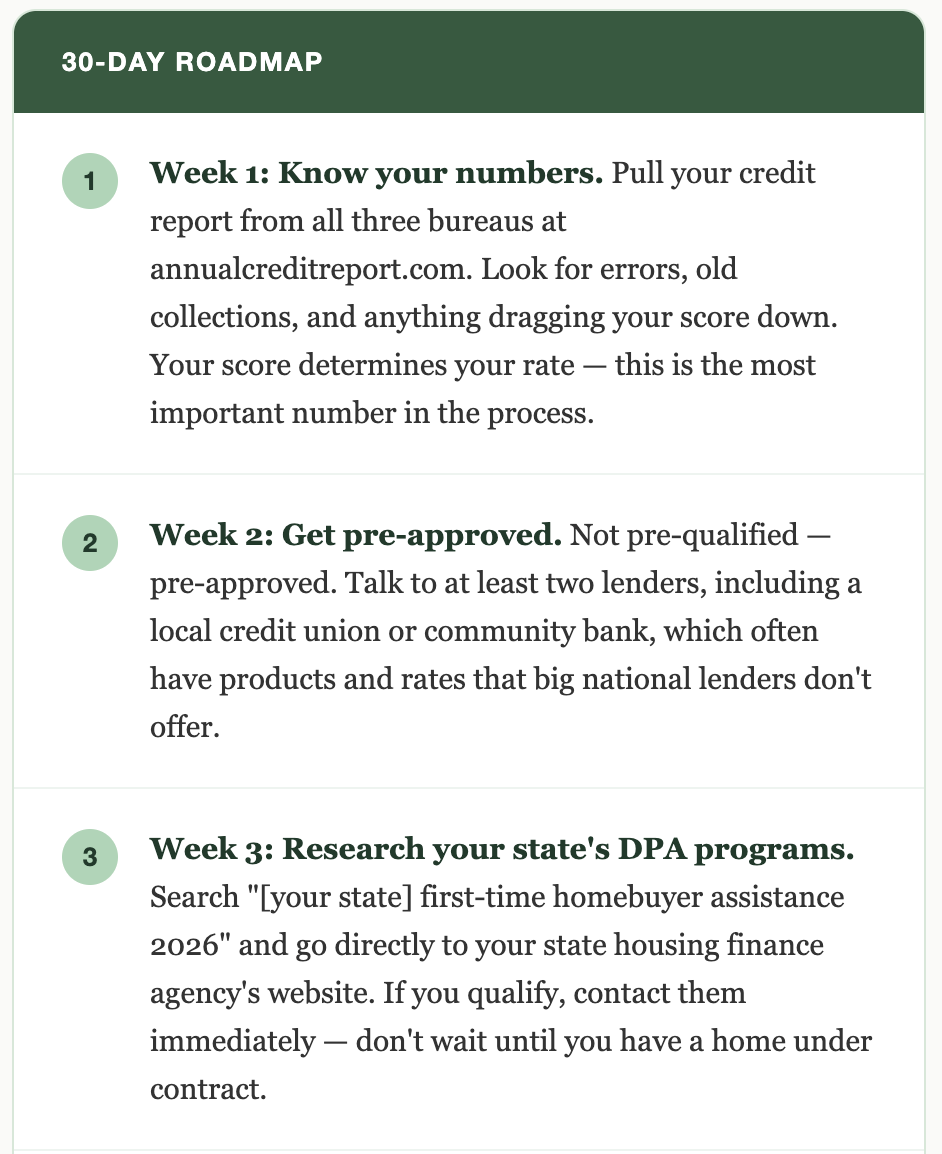

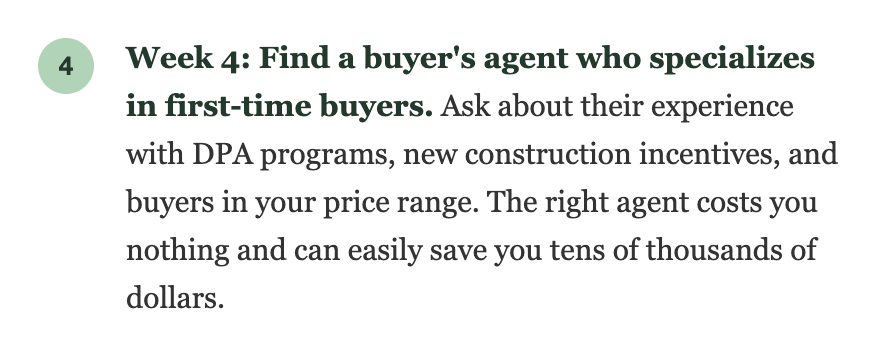

Your action plan: what to do in the next 30 days

The window is open. It won't stay that way forever.

Markets move in cycles, and this one has taken a long time to turn. Rate relief, rising inventory, aggressive DPA funding, and four years of rent increases have together created a moment that millions of renters have been waiting for — whether they knew it or not.

Maria, by the way, closed on a 3-bedroom home last month. Three percent down. A state grant covered her closing costs. Her monthly payment is $140 less than what her landlord wanted to charge her for the apartment.

She painted the kitchen green. She's not painting it back.

Ready to take the first step?

Talk to us! The best time to start is before you feel ready. ;)

-Team Taranto

Tom Taranto

Operator | Realtor® | Market Specialist | Taranto Team | Keller Williams Realty Brevard | PLACE

or another way